Occupancy rates and cash flow greatly profit the banking sector

Jun 6, 2024

Housing loans alone constitute over 60% of total outstanding loans in the Malaysian banking system.

Despite their apparent difference, the real estate and banking sectors are more in sync than one realises at first glance. Malaysian property plays a vital role in the country’s economic expansion and it fully depends on a delicate balancing act between bank profits and real estate management cash flow strategies with the success of one having a direct influence on the other.

The relationship between real estate management and banking profits is largely dependent on what is known as loan delinquency. Data from Bank Negara Malaysia (BNM) presents the residential property sector’s gross impaired loan (GIL) ratio as 1.8% in 2023. Even though this may only seem like a tiny portion, the non-performing loan balance amounts to billions of ringgit.

Painting the concerning picture

In a statement made by Prime Minister Datuk Seri Anwar Ibrahim, Malaysia boasts one of the highest household debt-to-GDP ratios globally, with an increase to 84.2% in 2023 compared to 82% in 2018. This makes up to RM1.53 trillion and the heavy debt is fueled in large part by the property sector. However, as of March 2024, the average lending rate for outstanding loans is 5.37% according to a report by BNM.

As per the Property Market Report 2023 published by the National Property Information Centre (Napic), there was a 7% decrease in the number of completed and unsold residential units from 27,746 units in 2022 to 25,816 units in 2023.

Additionally, the value of completed and unsold residential units decreased by 4%, from RM18bil to RM17.68bil in 2023. These completed and unsold units, primarily concentrated in high-rise condominiums, signifies a mismatch between supply and demand. According to BNM, as of the third quarter of 2023, housing loans alone constituted over 60% of total outstanding loans in the Malaysian banking system.

Overall, housing loans take up a significant portion of all loans currently active in Malaysia and with the current trajectory of active development project sites and Malaysians increasingly being unable to service their loans, it poses a worrying thought for the future.

How efficient real estate management helps

In addition to minimising maintenance expenses and preserving the property’s value, efficient property management guarantees on-time rental collections and consequently steady cash flow. Bank loan default risk is consequently reduced. Strong rental yields and well-kept properties draw in dependable tenants, which guarantees a consistent cash flow or income stream that helps borrowers pay off their debts.

In contrast, the problem of delinquency may worsen due to subpar property management strategies. Tenant and owner financial strain can result from neglected properties with low occupancy rates and growing maintenance costs. Repercussions for bank profitability and overall financial stability include an increased risk of loan defaults.

An incompetency case

In 2022, the National House Buyers Association (HBA) conducted a study which found that more than 60% of participants expressed dissatisfaction with the competency and transparency of their strata management committees. Property deterioration and falling property values can be caused by inadequate maintenance, ineffective maintenance fee collection and unresolved disputes within residential communities. The profitability of banks is impacted as a result of deterring potential customers and raising the possibility of loan defaults.

Collaboration is key

A collaborative approach is necessary to address the challenges. To ensure a greater degree of professionalism and accountability, regulatory bodies can impose stronger rules and training programs on strata management companies. Better financial reporting and decision-making procedures within strata committees can also build resident participation and trust, which will result in better-managed properties.

Open communication is crucial between property management firms, developers and banks. All parties involved can promote a more lucrative and sustainable ecosystem by collaborating to create and apply best practices. Furthermore, banks have been providing owners and developers with the means to maximise their assets by holding knowledge-sharing workshops and seminars on the significance of efficient property management.

Some strata management companies should also embrace technology. Many modern real estate management techniques utilising today’s applications see more streamlined business processes and well-informed decision-making processes. These solutions keep in check data analytics, tenant interactions and property management software to ensure things run smoothly.

In terms of transparency, creating a centralised property data repository and encouraging the use of standard accounting procedures are two initiatives that could greatly enhance banks’ ability to assess risk.

Ensuring long-term success

The correlation between banking profits and real estate management in Malaysia is complex. Despite the close relationship between the two, concentrating only on short-term gains can have negative long-term effects on both. To ensure the long-term success of both sectors, it is imperative to acknowledge this interdependence and strive towards a more professional and efficient property management landscape.

All parties involved can cooperate to guarantee a flourishing real estate market that supports a sound and successful banking system by placing a high priority on ethical property management techniques, encouraging openness and nurturing teamwork.

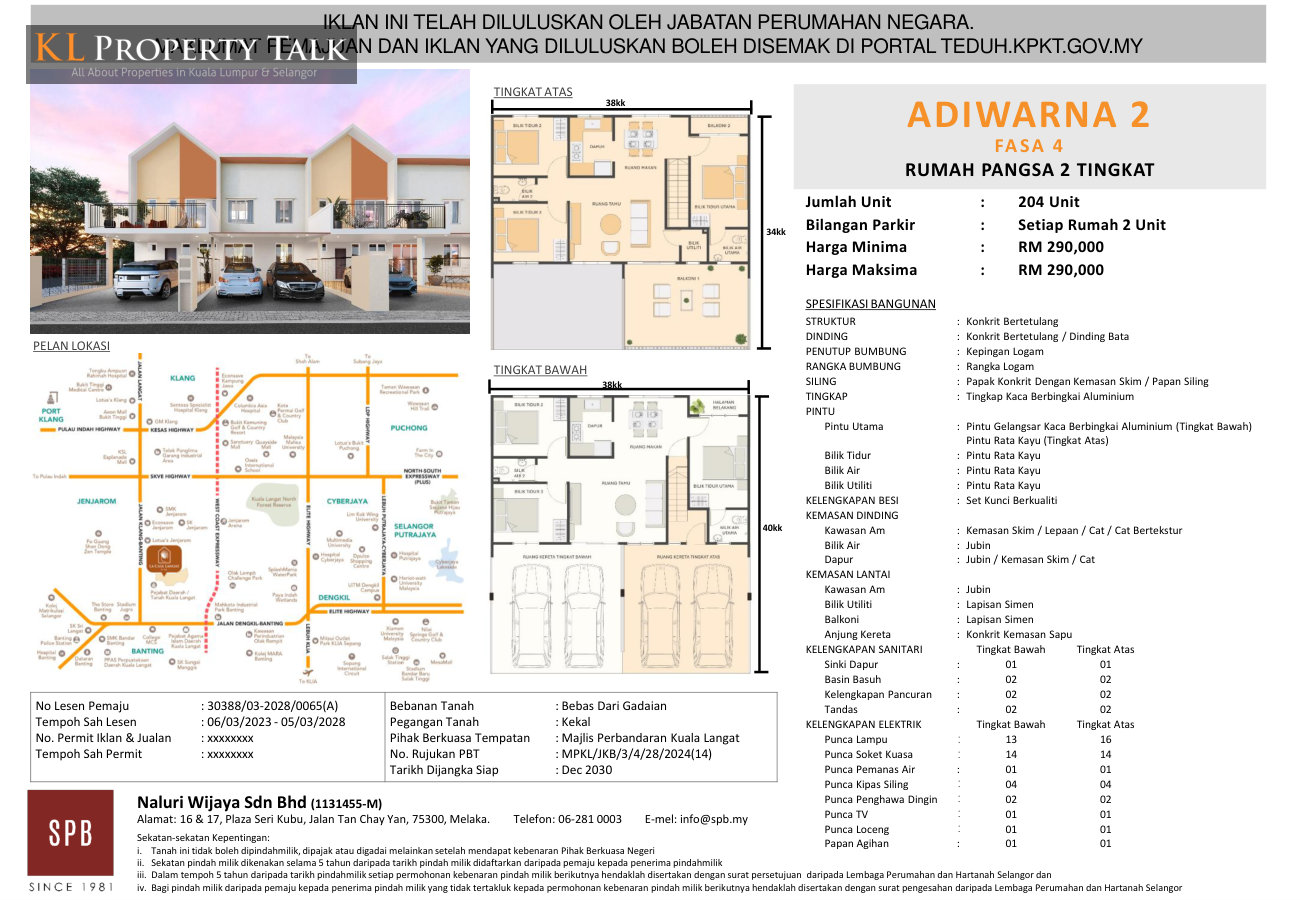

Adiwarna 2 is a thoughtfully planned residential development by SPB Property in Banting, Selangor, offering an affordable homeownership opportunity within...

POST YOUR COMMENTS