The Rent-to-Own is scheme is targeted at the B40 and M40 groups. (Rawpixel pic)

Under Budget 2021, it was announced that the government would work with selected financial institutions to provide a Rent-to-Own (RTO) scheme for 5,000 PR1MA homes at a total value of RM1 billion, especially for first-time homebuyers.

The proposed scheme has exempted stamp duty on the instruments of transfer between the developer and financial institutions, and between financial institutions and the prospective buyer.

The programme will kick off in 2021 and will continue throughout 2022. No official announcement has yet been made about applications and which financial institutions will be involved.

However, if you’re considering purchasing a home through the RTO scheme, now is the perfect time to do your research.

What is RTO and how does it work?

Although it has been around for decades in other countries, RTO is relatively new to Malaysia’s property market.

It is targeted mainly at homebuyers who do not have the credit scores to secure a loan. One of the main attractions of RTO is that no down payment is involved.

A lease agreement in an RTO scheme states a certain length of time that the buyer will rent the home for, usually five years or less. At the end of the agreed period, the buyer can either choose to purchase the property or walk away.

So, what is the difference between renting if you are paying but not owning the place anyway? The difference is that you do not need to come up with a hefty down payment, and you get to lock in the current market price of the property when you sign the contract, so you don’t need to worry about the price of the property going up.

Part of the money paid while renting can be converted into savings. (Pexels pic)

Part of the money you pay while renting can be converted into savings to help you settle the down payment when you decide to purchase, depending on the scheme you have chosen.

This is the reason you only need to have a deposit of three months’ rent instead of the usual 10% down payment.

Put simply, RTO can be thought of as a trial period when the buyer gets to experience living in the property.

At the same time, they get to fix their credit score and do whatever is necessary to obtain a loan to purchase the house.

Unfortunately, this means that if they fail to secure financing before the agreement ends, they either have to restructure the agreement or walk away.

The downside of RTO

First, you don’t actually own the property during the lease term. That means you cannot make any changes such as renovations without the owner’s approval.

Next, as mentioned above, you lock in the current market price when you sign the contract.

That means in the unlikely event the price of that particular project goes down, you are stuck with the higher, original purchase price.

Lastly, it is never good to delay or miss a payment, but with an RTO property the stakes are much higher.

Failing to comply with or breaching the terms of the agreement would forfeit all the money you have paid, leaving you both homeless and in debt.

If you just want to ‘try’ out a property, it would be better for you to rent traditionally. (Rawpixel pic)

Who is it for?

There are several RTO schemes available, but the better-known ones are PR1MA, Houzkey and Smart Sewa.

Some developers such as IOI Properties, SP Setia and Sime Darby offer their own RTO programmes, but projects by other developers may be available under the options of different financial institutions.

The different schemes have slightly different criteria, but in general, RTO is only open to Malaysian citizens or permanent residents who are at least 18 years old, who do not own more than one property or housing loan.

Other criteria include a minimum combined monthly income between you and your spouse but, not to worry, if your income is not high enough you can bring in guarantors to ensure that your rent does not go unpaid.

RTO schemes were created with the B40 and M40 groups in mind, specifically to reduce the initial cost of buying a home.

It allows first-time homebuyers who cannot pay the 10% down payment, and first-time homebuyers who are still working on building their credit score, to save up and fix their financial habits while knowing the exact amount they have to pay for the house.

In a nutshell, if your heart is set on purchasing a home in a certain project, but you cannot afford the down payment, RTO would be good for you as you get to live in the property immediately.

However, if you just want to “try” out a property, it would be better for you to rent traditionally.

This article was written by Adlene Hanna of PropertyAdvisor.my, Malaysia’s most comprehensive source of property data, property analytics and insights.

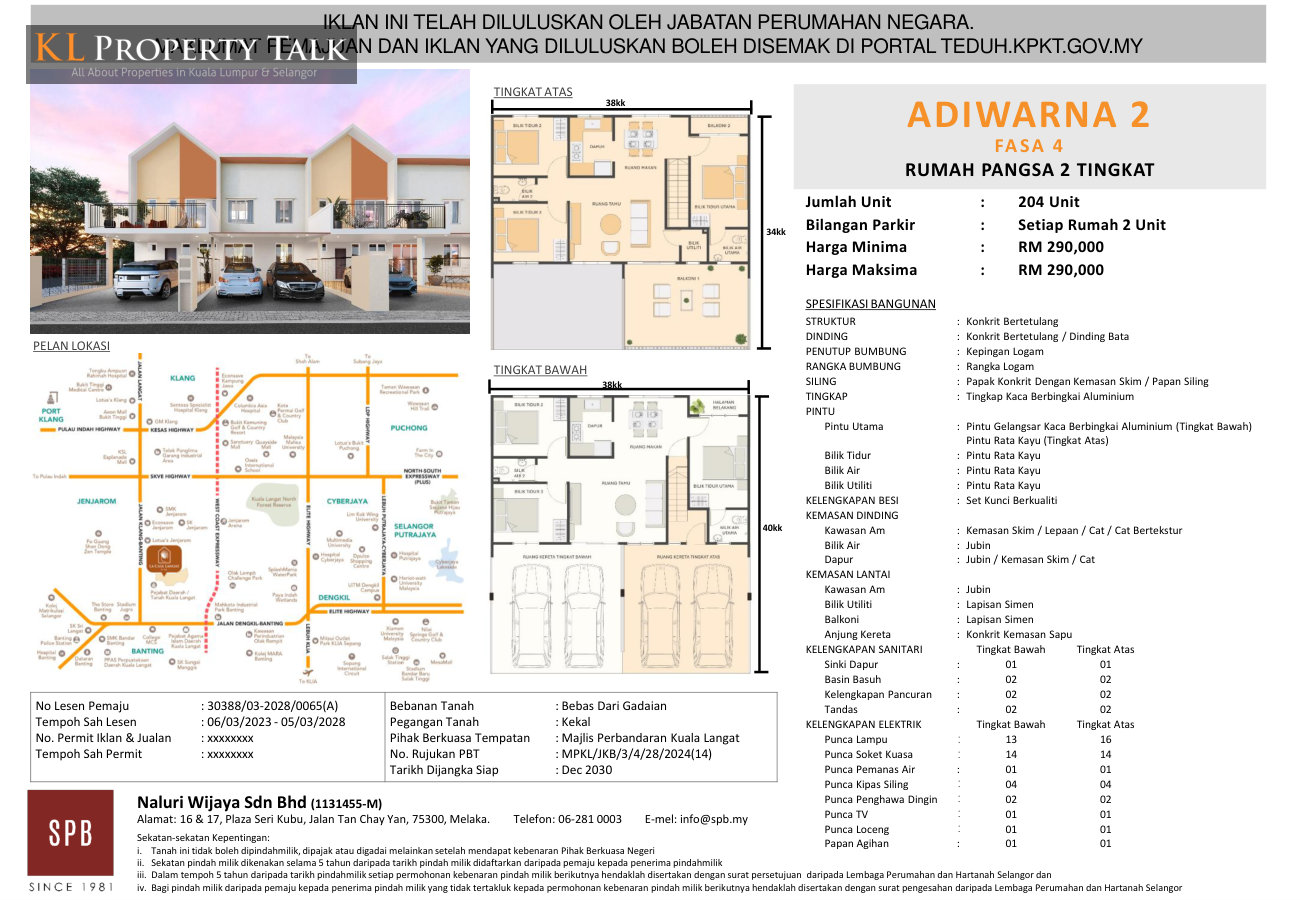

Adiwarna 2 is a thoughtfully planned residential development by SPB Property in Banting, Selangor, offering an affordable homeownership opportunity within...

POST YOUR COMMENTS