Top view of 2025 number written on the wall look through magnifying glass

A deep dive into a year of resilience and regulatory shift

By Joseph Wong

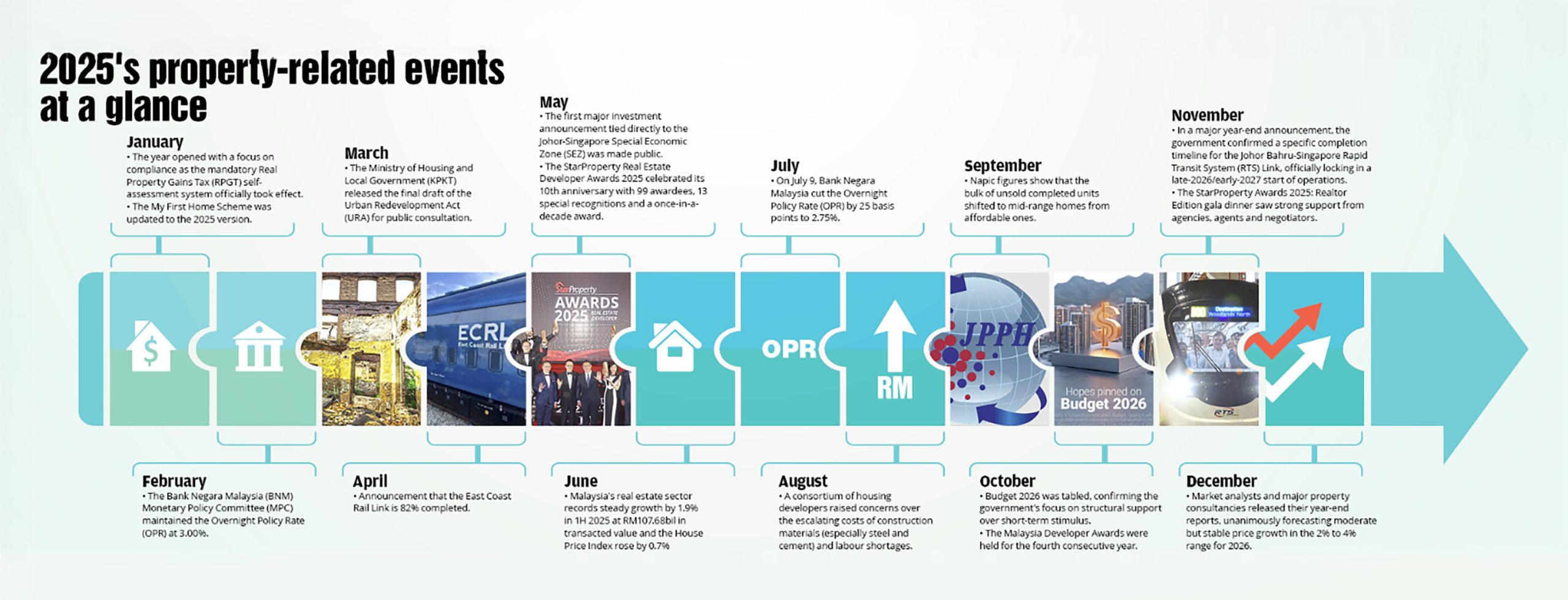

The year 2025 has cemented its place as a pivotal period for the Malaysian property market, marking a transition from post-pandemic recovery to regulatory maturity. The market dynamics were characterised by a curious divergence which witnessed a demonstration of strong transactional resilience in value terms, even as volume metrics remained subdued.

This resilience, however, was accompanied by persistent challenges, chief among them the ongoing struggle for affordability and the necessary adaptation to significant, mandatory government policy changes, particularly the introduction of the Real Property Gains Tax (RPGT) self-assessment system.

The first half of the year saw the total value of property transactions rise robustly by 1.9% to RM107.68bil. This growth in transactional value is a testament to the underlying demand for quality real estate and inflationary pressures within the construction sector. The market effectively shrugged off global uncertainties, reflecting strong domestic liquidity and confidence, especially among high-net-worth individuals and institutional investors.

However, this growth in value was achieved despite a slight dip in the total number of property deals transacted. This divergence—value rising while volume falls—is symptomatic of several key factors:

Rising asset prices: Inflationary costs for construction materials (cement, steel, labour) are consistently passed on, increasing the average selling price of new launches.

Secondary market strength: The secondary market, particularly for established properties in prime areas with readily available infrastructure, saw strong price appreciation, contributing heavily to the overall rise in transaction value.

Affordability bottleneck: The primary reason for the stagnant volume lies in the widening gap between house prices and median household income, pushing first-time buyers and B40/M40 segments out of the market for certain housing types.

The overall outlook for the remaining quarter of 2025 remains cautiously optimistic. This positive sentiment is underpinned by continued economic recovery, sustained political stability and the tangible progress of critical national infrastructure projects that act as economic catalysts.

Addressing structural challenges

While high transaction values suggest a healthy market, the sector cannot ignore two critical, long-standing pressures, namely, the current level of unsold completed units and the affordability crisis.

The build-up of unsold units—defined as completed properties that have remained unsold for more than nine months—continues to plague specific segments. Geographically, the crisis is disproportionately severe in certain states and heavily concentrated in high-rise residential properties priced above the RM500,000 threshold. For developers, this represents trapped capital and necessitates significant inventory management strategies, often involving heavily discounted bulk sales or the temporary conversion of stock into rental-only assets.

The affordability challenge is perhaps the most pressing socio-economic issue in the property market. Government schemes like the My First Home Scheme 2025 and specific financial aid for low-income households are crucial stop-gap measures. However, a sustainable solution requires a systemic approach to control construction inflation, simplify regulatory approval processes to reduce developer costs and increase the supply of genuinely affordable, strategically located housing.

Major regulatory shift

Effective Jan 1, 2025, the property market underwent a foundational regulatory change with the mandatory implementation of the RPGT self-assessment system. This single change fundamentally altered the mechanics of property disposal.

Previously, the administrative burden of calculating and submitting RPGT lay primarily with the buyer’s solicitor and the Inland Revenue Board (LHDN). Now, the onus is placed entirely on the seller to accurately determine their chargeable gains and ensure timely payment of the tax liability.

Impact and compliance risks

The move aims to enhance tax efficiency and minimise arrears but it introduces several critical implications for stakeholders:

Seller responsibility: Sellers must now fully understand their acquisition costs, disposal price and qualifying expenses (eg renovation and legal fees) to calculate the correct tax. Mistakes or omissions can result in hefty penalties.

Professional reliance: The demand for professional tax agents and lawyers specialising in property tax compliance has surged. The complexity of calculating RPGT—which depends on the ownership period (ranging from five or more years) and the asset type (residential vs commercial)—requires expert guidance to ensure legal compliance.

Transaction timelines: While the process theoretically speeds up the LHDN’s internal processing, the initial period of self-assessment implementation has introduced a need for meticulous due diligence on the seller’s side, sometimes extending the initial stages of transaction finalisation.

This self-assessment system represents a significant step towards modernising the tax framework, requiring all market participants to operate with greater accountability and transparency.

Infrastructure and budgetary support

The government’s strategic commitment to large-scale infrastructure acts as a vital booster for the property market, transforming previously remote areas into lucrative development corridors.

The East Coast Rail Link (ECRL) is the clearest example of a catalytic project. With an impressive 82% completion rate reported as of April 2025, the ECRL is no longer a future prospect but a near-term reality. The project is reshaping the economic landscape of the East Coast states (Kelantan, Terengganu and Pahang) and transforming transit times to the West Coast hubs. The property market, in anticipation, is already seeing speculative investments and increased development planning around future ECRL stations, particularly in the transit-oriented development (TOD) clusters they enable.

Furthermore, the Budget 2025 Initiatives provided specific injections of support:

RM3bil for industrial infrastructure: This allocation for upgrading infrastructure in industrial parks is crucial for attracting high-value manufacturing and logistics, thereby creating job opportunities that, in turn, drive residential demand in surrounding areas.

Stamp duty exemptions: The targeted stamp duty exemptions for SMEs purchasing commercial properties below RM2mil are a direct mechanism to support business expansion and commercial real estate transactions, which have lagged behind the residential segment.

Urban redevelopment and evolving demand

Looking ahead, the market’s trajectory is heavily influenced by planned legislative action and fundamental shifts in buyer preferences.

The government’s active formulation of a new Urban Redevelopment Act (URA) is potentially the most significant long-term policy move. The URA aims to address the challenge of ageing and dilapidated buildings, particularly within densely populated urban centres like Kuala Lumpur. Currently, consensus requirements (often needing 100% owner approval for demolition/redevelopment) are a major impediment to urban renewal. The proposed URA is expected to lower this threshold, facilitating the much-needed redevelopment of brownfield sites.

However, the URA presents its own set of complexities, including:

Consensus mechanism: Determining the appropriate majority threshold (eg 75% or 80%) that balances development needs with individual property rights. This is perhaps the biggest setback for the URA proposal as it had resulted in much negative feedback.

Strata management: Navigating the intricate legalities and ownership structures of existing strata properties.

Compensation framework: Establishing a fair and transparent compensation model for displaced residents and business owners.

Nevertheless, a successful implementation of the URA will be key to ensuring Kuala Lumpur’s competitive edge as a modern, high-density city, provided all the underlying issues are ironed out.

Buyer trends: Smart, green and connected

Contemporary buyers are increasingly sophisticated, with purchasing decisions guided by factors beyond mere location and size.

Smart and sustainable homes: Demand for properties that incorporate Environmental, Social and Governance (ESG) principles is soaring. This includes homes with energy-efficient designs, smart home technology for optimised utility consumption and access to renewable energy sources. Sustainability is rapidly moving from a niche preference to a mainstream expectation.

Transit-Oriented Developments (TODs): The integration of housing, commercial spaces and public transportation hubs continues to command premium pricing. TODs cater to a generation prioritising convenience, reduced commute times and a car-lite lifestyle, making them highly strategic investments.

The Malaysian property market in 2025 is demonstrating a robust, if uneven, maturity. The growth in transaction value signals underlying strength while the continued focus on affordable housing and the strategic roll-out of infrastructure projects like the ECRL provide solid foundations for future expansion. The mandatory RPGT self-assessment and the forthcoming Urban Redevelopment Act underscore the government’s commitment to structural reform and a more efficient, transparent market.

As the industry moves into 2026, the key to sustained growth will be the effective navigation of regulatory compliance and the success of the URA in unlocking prime urban land for renewal, ultimately balancing the twin goals of market value growth and genuine housing affordability for all segments of the population.

PETALING JAYA: Malaysia’s property developers remain cautiously optimistic about the market outlook for 2026, although global geopolitical tensions could dampen...

POST YOUR COMMENTS