Schemes and benefits for first home buyers in

Malaysia

Dec 29, 2020

The government is going all out to increase homeownership with various schemes and benefits under Budget 2021 targeted to first home buyers. (Rawpixel pic)

With the government’s various incentives to increase homeownership under Budget 2021, there’s no better time than now to purchase a home, especially if you’re a first-time home buyer.

Whether it’s full financing or affordable prices, it’s a lot less costly to purchase your first home if you do your due diligence and find out exactly how you can benefit as a first home buyer (FHB).

Here is a simple list to get you started.

1. FHB enjoy full stamp duty exemption until 2025

That’s right, if you’re a FHB who can’t afford to buy a home just yet, you still have five years to plan your finances.

FHBs who purchase residential properties between Jan 1, 2021 to Dec 31, 2025 will enjoy stamp duty exemption for their memorandum of transfer (MOT) and loan agreements.

This is under the condition that the Sales and Purchase Agreement (SPA) is executed and signed within the aforementioned period. The discount applies for properties priced up to RM500,000.

Under the National Economic Recovery Plan called Penjana announced in June 2020, stamp duty exemption was originally limited to newly launched projects.

However, under the newly approved Budget 2021, stamp duty exemption is now extended to the secondary market, which gives FHBs more options in their house-hunting quest.

For context, stamp duty is calculated based on the price of the property. The first RM100,000 incurs a stamp duty of 1% and the next RM400,000 will cost 2% of the total property price.

There is also a 0.5% stamp duty on your loan agreement, based on the flat rate of your total loan.

Sample calculation of stamp duty for a house priced at RM500,000:

{(First RM100,000 x 1%) + (Next RM400,000 x 2%)} + 0.5% of loan amount (90% of RM500,000)

The government has allocated RM1 billion under Budget 2021 for the PR1MA rent-to-own programme.

2. Introduction of rent-to-own PR1MA homes

Also, under Budget 2021 is PR1MA’s rent-to-own programme with an allocation of RM1 billion.

Created specifically for FHBs, this programme involves 5,000 PR1MA properties and will run from 2021 until 2022. The list of financial institutions involved and full details of the programme is yet to be announced.

Generally, a rent-to-own scheme is ideal for youth who have yet to build up a credit score to qualify for a home loan and those who do not have the funds required for a down-payment.

Essentially, under a rent-to-own scheme, a buyer will first rent the property at a rate slightly higher than market price. At the end of the contract, the buyer can then choose to purchase the property from the developer.

The difference between rent-to-own and a regular rental or property purchase is that the buyer gets to lock in the current purchase price when they first sign the contract.

This means that even if the market price has gone up since they started renting, they still pay the same price that they would have paid if they had bought the house immediately.

Additionally, part of the rent paid can be converted towards the down-payment.

Under the My First Home Scheme, all Malaysian FHBs without any record of impaired financing for the past 12 months are eligible to apply.

Under the My First Home Scheme, all Malaysian FHBs without any record of impaired financing for the past 12 months are eligible to apply.

3. Introduction of My First Home Scheme (Skim Rumah Pertamaku, SRP)

This scheme was first announced in Budget 2011 to assist FHBs towards owning a home without having to pay a down payment.

Participating financial institutions may provide up to 110% financing to FHBs with a gross monthly household income of up to RM10,000. For individual applicants, the maximum income is capped at RM5,000.

According to the official SRP website, all Malaysian FHBs without any record of impaired financing for the past 12 months are eligible to apply, whether they are a salaried worker or self-employed.

SRP covers residential properties of up to RM500,000 in both primary and secondary markets. It is also applicable for properties that are still under development.

The financial tenure must not exceed 35 years and the buyer must not exceed 70 years of age at the end of the tenure.

There is also a mandatory online financial education module provided by AKPK for FHB of property priced up to RM300,000 and with a monthly gross household income of not more than RM5,000.

4. Introduction of Rumah Selangorku and Residensi Wilayah

These two schemes are specially for residents of Selangor and the Federal Territories, respectively.

Like the above schemes, they were set up to assist FHBs towards homeownership at reasonable rates within their state of residence.

Led by Lembaga Perumahan dan Hartanah Selangor (LPHS), Rumah Selangorku was first introduced in 2014 to encourage and support developers to produce affordable homes. As such, properties available under the scheme are all below RM250,000.

Similarly, Residensi Wilayah, formerly known as RUMAWIP, is a project that offers properties in the Federal Territories at a maximum price of RM300,000.

The minimum age requirement for Rumah Selangorku is 18 years, while for Residensi Wilayah, applicants must be at least 21 years old.

In terms of income, the maximum household income for Rumah Selangorku is set at RM10,000 whereas for Residensi Wilayah, the maximum income is RM15,000 for married couples and RM10,000 for individuals.

Only one application per household is allowed for both schemes.

This article was written by Adlene Hanna of PropertyAdvisor.my, Malaysia’s most comprehensive source of property data, property analytics and insights.

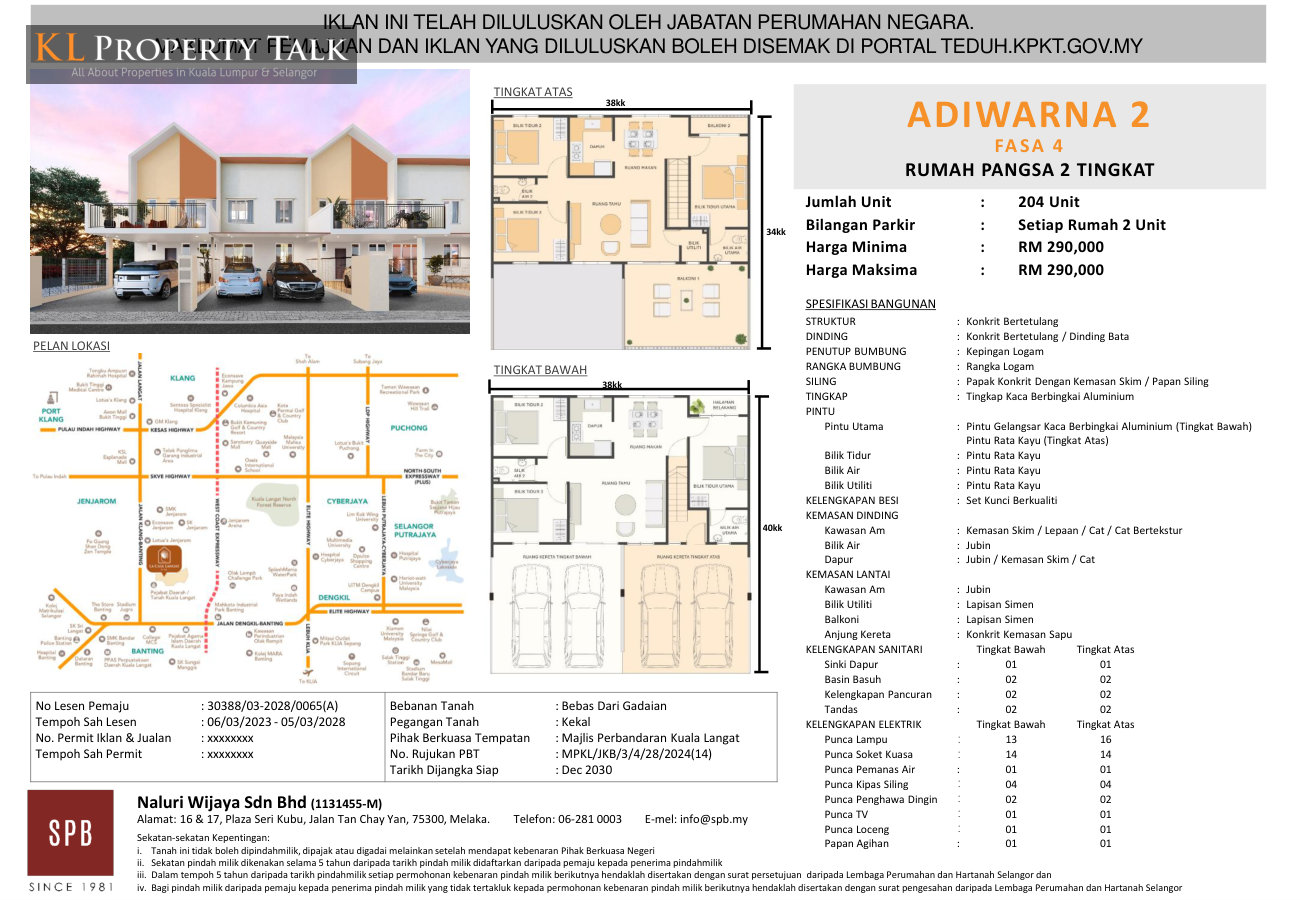

Adiwarna 2 is a thoughtfully planned residential development by SPB Property in Banting, Selangor, offering an affordable homeownership opportunity within...

POST YOUR COMMENTS