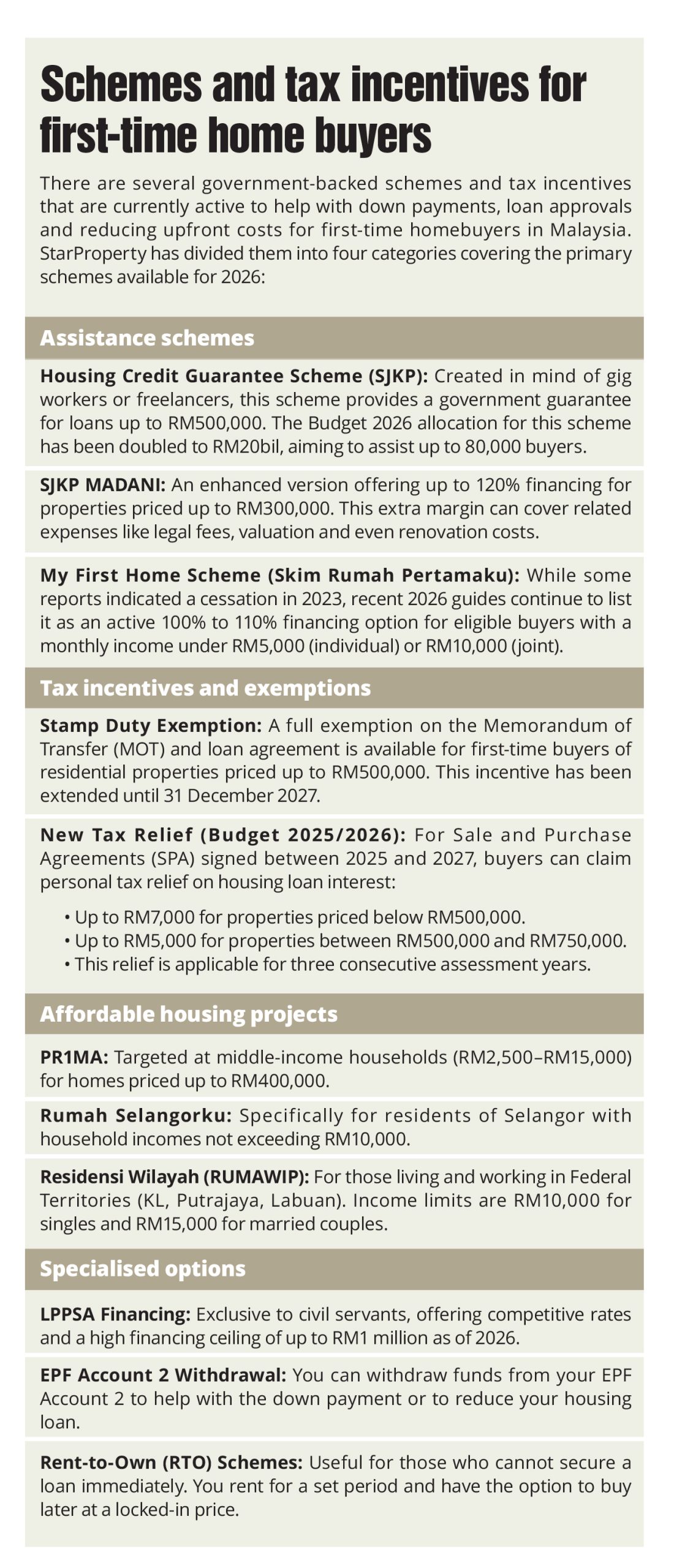

Navigating the first home ownership

From

| 10/04/2026

Rising costs push developers toward lifestyle-driven housing The idea that a fresh graduate can afford a 2,500 sq ft terrace...

Read More

Navigating buyer eligibility in Malaysia’s 2026 property market

By Joseph Wong

In the high-stakes arena of real estate, the transition from browsing to owning is governed by a singular, formidable concept: Eligibility. As Malaysia navigates the landscape of 2026, the definition of an eligible buyer has evolved far beyond a simple bank balance.

Today, eligibility is a sophisticated, multi-layered digital assessment, functioning like a gatekeeper that determines not only if one is legally permitted to own a specific title but also whether the financial institutions of the future trust the potential borrower with their capital.

For the modern home buyer, understanding this framework is the difference between securing a dream asset and facing the heartbreak of a rejected application. These criteria have become increasingly digitised, deeply integrated with sustainability metrics and more focused on granular credit health than ever before. To master the market, one must view eligibility through two distinct lenses: Legal permission and financial trust.

Legal eligibility: The right to own

Legal eligibility is the first hurdle, dictated by the Malaysian government and project developers. It is the regulatory framework that determines what a person is allowed to own based on his or her identity, citizenship and current asset portfolio.

Nationality remains the primary filter. Malaysians enjoy the broadest spectrum of access, able to purchase almost any property type, including the coveted bumiputera quota units, which offer significant discounts, provided they meet the specific ethnic criteria.

Foreigners, however, navigate a more complex terrain. Under the 2026 guidelines, the government has introduced a 8% flat stamp duty for non-citizens to curb speculative heat. Furthermore, strict price floors remain in effect to protect the local supply. While the standard threshold is generally RM1mil and above, specific strategic zones like Forest City in Johor or regions like Sarawak offer lower entry points to encourage international investment. However, certain red lines remain. Foreigners are strictly barred from low-cost housing.

The first-time buyer shield

To combat the rising cost of living, 2026 sees a fortification of first-time buyer status. Schemes like the MyFirst Home Scheme (SRP) are exclusive to those who have never held a residential title. This eligibility is verified instantly via the integrated digital land registry, making proxy purchases or hidden titles impossible to conceal.

Eligibility is also a tool for social engineering. Affordable housing schemes, such as PR1MA or RUMAWIP, utilise ceiling income limits. These are designed to ensure that subsidised rates benefit those truly in need. If the household income exceeds the bracket, even by a small margin, the applicant is legally deemed ineligible.

Financial eligibility: Through a bank’s lens

While the government decides if an individual or corporation can buy, the banks decide if they can afford it. From a bank’s perspective, eligibility goes far beyond approval. It is fundamentally about risk sustainability over the next 30 to 35 years. A mortgage is a long-term commitment. “For banks, assessing buyer eligibility means evaluating not just whether a borrower can afford instalments today but whether they can continue servicing the loan through economic cycles, interest rate fluctuations and life changes.

“At its core, financial eligibility rests on three pillars, namely, repayment capacity, credit behaviour and transaction risk. Repayment capacity is measured through the borrower’s income stability and Debt Service Ratio (DSR). Banks assess net income after statutory deductions and existing commitments to determine how much buffer a customer truly has.

“Credit behaviour is reviewed via CCRIS records and repayment history. A clean and consistent payment track record signals financial discipline, which lowers default risk,” said a bank contact.

She added that transaction risk refers to the property itself, namely, its valuation, location, liquidity and market demand. A well-located property with strong secondary market appeal carries lower risk than speculative or oversupplied developments.

Financial eligibility is governed by the Debt Service Ratio (DSR) and the Margin of Finance (MOF). The DSR is one’s financial report card. It is the calculation of a borrower’s total monthly debt such as car loans, credit cards, PTPTN and personal loans against the net monthly income. In the current lending environment, banks have tightened the screws. Most institutions now demand a DSR below 60–70%.

In the digital-first banking era of 2026, banks use real-time AI to scan applicants’ CCRIS and CTOS reports. A good credit score is no longer just about the amount owed but the discipline with which the monthly repayment is settled. A single missed credit card payment or a late utility bill in the last 12 months can trigger an automated rejection.

The borrowers’ eligibility for a loan amount is also tied to their history. For first and second homes, most buyers still qualify for 90% financing. However, the Third Home Rule remains a significant barrier. For the third residential property onwards, eligibility drops to 70%. This shift requires the buyer to have significantly higher cash reserves, effectively separating the casual investor from the institutional-level player.

The developer’s perspective

To understand how these eligibility layers impact the supply side, StarProperty turned to Real Estate and Housing Developers’ Association (Rehda) president Ho Hon Sang. From the developer’s viewpoint, buyer eligibility is not just a hurdle. It serves as a blueprint for how they design and market their products.

According to Ho, developers categorise eligibility into three core demographics:

How do developers respond to these groups? “There is no great distinction in the way developers react to these market groups, though specific types of residential units and their locations may be more appealing to a specific group than others. As such, the marketing strategy may cater to the group they want to attract,” said Ho.

“First-time youth buyers, for example, may be more inclined to choose homes that cost RM500,000 while the marketing side will focus on the property’s accessibility and proximity to business or commercial centres and transportation hubs. Meanwhile, higher-end products may be made more attractive to those looking to buy property for their elders by focusing on their distance from the chaos of city life while remaining in proximity to the city,” he added.

Eligibility as empowerment

Whether a buyer is a first-timer seeking a foothold in an urban hub or an investor looking to capitalise on Johor’s booming economy, the key to success lies in preparation.

By understanding the government’s legal boundaries and the bank’s financial expectations, a home buyer transitions from being a passive seeker to a qualified buyer. As Ho and Rehda emphasised, the property market is the foundation of the nation’s society and navigating one’s eligibility is simply the first step in building one’s place within that foundation.

Source: StarProperty.my

POST YOUR COMMENTS