Strategies to overcome market abuses

From

| 16/03/2026

By Datuk Mani Usilappan The findings of the 2026 economic review are unequivocal: While Malaysia has rightfully earned its status...

Read More

By Joseph Wong

The first quarter of 2026 has been defined by noise. From chaotic shifts in international trade routes to the volatile swings of the oil market, the external environment has been anything but predictable. Yet, on March 5, Bank Negara Malaysia (BNM) sent a powerful signal of domestic calm by maintaining the Overnight Policy Rate (OPR) at 2.75%.

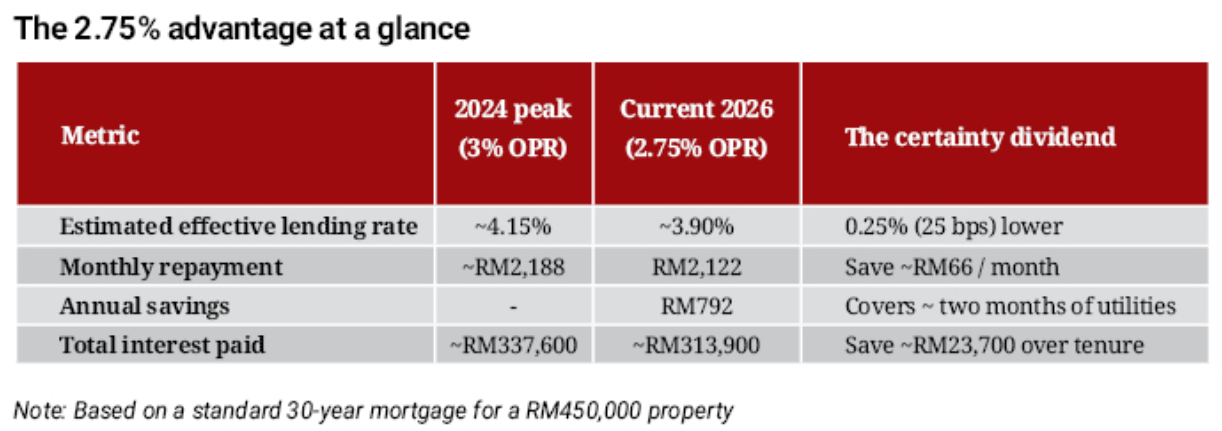

For the Malaysian property buyer, this decision is likened to a certainty dividend. In a market where affordability is the primary gatekeeper to home ownership, the central bank’s commitment to stability is providing the financial breathing room necessary for a new generation of buyers to enter the market with confidence.

According to Juwai IQI co-founder and group chief executive officer Kashif Ansari, the Monetary Policy Committee’s (MPC) decision to hold rates reflects a calculated focus on domestic resilience. While the US dollar has surged and global trade faces an unpredictable tariff landscape, BNM has opted for a stance of calculated patience.

“International markets have been surprisingly stable despite what has been going on,” Ansari noted. “The biggest financial impact of global events this week has been the surge in the US dollar and the price of oil. We don’t know if these conditions will continue over the long term but for this week’s decision, we see no impact. If they were to do so, that could have an impact on Bank Negara’s future decisions about interest rates but all that is speculative.”

Rather than reacting to external volatility, BNM is prioritising internal metrics, namely, inflation and growth. By keeping the OPR at 2.75%, the central bank is effectively shielding the Malaysian homebuyer from the interest rate shock that has paralysed property markets in more reactive economies.

Malaysia’s exceptionally strong position

The justification for this stability lies in Malaysia’s macroeconomic health. As we move further into 2026, analysts are projecting a robust GDP growth of 4.5%. Perhaps most impressively, inflation has remained remarkably tame. January reports showed headline inflation at a steady 1.6% while housing costs, the most critical metric for the real estate sector, rose by a modest 1.2%.

“Until this week, analysts expected the MPC to leave interest rates unchanged throughout the rest of 2026,” said Ansari. “That remains our expectation today. While sustained higher oil prices or a flight of capital could prompt a future move, as of today, we believe those possibilities to be unlikely.”

The borrower’s cheat sheet

To understand why a stable 2.75% OPR is such a win for the consumer, we must look at the direct impact on monthly cash flow. The difference between the 3% peak of 2024 and the current 2.75% equilibrium is significant when projected over a standard 30-year mortgage.

As Ansari explained, even a 25-basis-point shift can alter the trajectory of a household’s finances. RM60 to RM70 per month isn’t a dramatic amount in isolation but it directly affects loan eligibility. By holding the rate, the bank ensures that more Malaysians stay within the Debt Service Ratio (DSR) limits required for approval.

The road to equilibrium

To appreciate the current stability, one must look back at the post-Covid recovery. In 2022 and 2023, BNM was forced to raise rates several times to curb inflationary pressures, eventually reaching a peak of 3.00%.

The turning point came in July 2025, with a historic 25-basis-point cut to 2.75% which was the first reduction in five years. This cut was a normalisation signal, suggesting that the Malaysian economy had successfully navigated the post-pandemic turbulence. “Since that cut, Bank Negara has been able to keep inflation under control and below historic levels. Thus, the bank has left the overnight policy rate unchanged, supporting sustainable economic and property market growth,” Ansari said.

Real estate impact

This interest rate environment has created a unique Goldilocks scenario for the Malaysian real estate market. It is warm enough to encourage healthy transaction activity but cool enough to prevent speculative bubbles. Moreover, steady activity is currently being observed in Malaysia’s Golden Triangle of growth:

Importantly, developers have remained disciplined. “There is no evidence of overheating or increasing oversupply. Loan approval rates remain healthy and household debt growth has slowed significantly from the early 2020s,” Ansari noted.

The strategy of continuity

As the Malaysian property market matures in 2026, the OPR decision serves as a reminder that the best incentive for a buyer isn’t a temporary developer rebate but a stable and predictable financial environment.

“In short, we expect Bank Negara Malaysia’s Monetary Policy Committee to leave the Overnight Policy Rate unchanged at 2.75%. Domestic conditions justify this patience, and for now, we see no reason for the committee to change its stance. The most likely outcome is continuity. That will support households, businesses and the property market,” said Ansari.

For the buyer standing on the sidelines, the message is clear. The floor has been set, the rates are stable and the certainty dividend is ready to be claimed.

This article was first published in StarBiz 7.

Source: StarProperty.my

POST YOUR COMMENTS